4QFY2017 Result Update | Pharmaceutical

June 12, 2017

Sun Pharma

BUY

CMP

`525

Performance Highlights

Target Price

`712

(` cr)

4QFY2017

3QFY2017

% chg (qoq)

4QFY2016

% chg (yoy)

Investment Period

12 months

Net sales

6,825

7,683

(11.2)

7,414

(7.9)

Sector

Pharmaceutical

Other income

536

352

52.6

185

189.4

Market Cap (` cr)

1,25,916

Gross profit

4,630

5,435

(14.8)

5,962

(22.3)

Net Debt (` cr)

(8,242)

Operating profit

1,235

2,224

(44.4)

2,300

(46.3)

Beta

0.7

Adj. Net profit

1,385

1,722

(19.5)

1,714

(19.2)

52 Week High / Low

855/493

Source: Company, Angel Research

Avg. Daily Volume

1,78,292

For 4QFY2017, Sun Pharma posted tepid numbers. For the quarter, the sales came in at

Face Value (`)

1

`6,825cr v/s. `7,600cr expected, registering a yoy dip of 7.9%. India sales at `1,916cr,

BSE Sensex

31,262

were up by 10% as compared to 4QFY2016, US finished dosage sales at US$381mn

Nifty

9,668

down by 34% vis-à-vis 4QFY2016. On the OPM front, the gross margins came in at

Reuters Code

SUN.BO

67.8% v/s. 80.4% in 4QFY2016, which lead the EBDITA margins to come in at 18.1% (v/s.

Bloomberg Code

SUNP@IN

31.1% expected) v/s. 31.0% in 4QFY2016. Despite the sharp dip in margins, the higher

other income at `536cr v/s. `185cr in 4QFY2016, lead the Adj. net profit to come in at

`1,385cr v/s. `1,433cr expected, a yoy dip of 19.2%. We maintain our Buy.

Shareholding Pattern (%)

Promoters

54.4

Results lower than expectations: India sales at `1,916cr, were up by 10% as compared to

MF / Banks / Indian Fls

16.0

4QFY2016, US finished dosage sales at US$381mn down by 34% vis-à-vis 4QFY2016.

FII / NRIs / OCBs

21.6

Emerging Markets sales at US$181mn was up 46% over 4QFY2016. Rest of World sales

Indian Public / Others

8.0

at US$109mn grew

38% over 4QFY2016. This growth was partly driven by the

consolidation of the Japan business. On the OPM front, the gross margins came in at

67.8% v/s. 80.4% in 4QFY2016, which lead the EBDITA margins to come in at 18.1% (v/s.

Abs. (%)

3m 1yr

3yr

31.1% expected) v/s. 31.0% in 4QFY2016. Despite the sharp dip in the margins, the

Sensex

8.1

16.8

22.2

higher other income at `536cr v/s. `185cr in 4QFY2016, lead Adj. net profit to come in at

Sun Pharma

(23.4)

(29.3)

(12.7)

`1,385cr, a yoy dip of 19.2%.

Outlook and valuation: Sun Pharma is one of the largest and fastest growing Indian

pharmaceutical companies. We expect its net sales to post a CAGR of 9.7% (including

Ranbaxy Laboratories) to `36,451cr and EPS to come in at `32.3 over FY2017-19E. We

recommend a Buy rating on the stock.

3-year price chart

1,200

Key financials (Consolidated)

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

1,000

Net sales

27,888

30,264

32,899

36,451

800

% chg

2.2

8.5

8.7

10.8

600

Adj. Net profit

6,248

7,846

7,580

7,760

400

% chg

31.7

25.6

(3.4)

2.4

EPS (`)

200

26.0

32.7

31.6

32.3

EBITDA margin (%)

24.6

29.0

26.9

25.4

P/E (x)

20.2

16.0

16.6

16.2

Source: Company, Angel Research

RoE (%)

21.0

22.2

18.7

18.8

RoCE (%)

15.6

18.8

16.9

15.1

P/BV (x)

3.8

3.4

2.9

2.5

Sarabjit Kour Nangra

EV/Sales (x)

+91 22 39357600 Ext: 6806

4.4

3.9

3.5

3.0

EV/EBITDA (x)

17.7

13.6

13.1

11.9

Source: Company, Angel Research; Note: CMP as of June 9, 2017

Please refer to important disclosures at the end of this report

1

Sun Pharma | 4QFY2017 Result Update

Exhibit 1: 4QFY2017 performance (Consolidated)

Y/E March (` cr)

4QFY2017

3QFY2017

% chg QoQ

4QFY2016

% chg yoy

FY2017

FY2016

% chg

Net sales

6,825

7,683

(11.2)

7,414

(7.9)

30,264

27,888

8.5

Other income

536.4

351.6

52.6

185.3

189.4

1,902

1,257.2

51.3

Total income

7,362

8,035

(8.4)

7,599

(3.1)

32,166

29,145

10.4

Gross profit

4,630

5,435

(14.8)

5,962

(22.3)

22,133

21,558

2.7

Gross margin (%)

67.8

70.7

80.4

73.1

77.3

Operating profit

1,235

2,224

(44.4)

2,300

(46.3)

8,810

6,874

28.2

Operating margin (%)

18.1

28.9

31.0

29.1

24.6

Interest

45

167

(73.0)

89

(49.2)

400

523

(23.6)

Depreciation

338

307

10.2

264

27.9

1,265

1,038

21.9

Extraordinary item loss/ ( gain)

0

0

0

0

-590

PBT

1,389

2,102

(33.9)

2,132

(34.9)

9,048

6,571

37.7

Provision for taxation

44.3

372.9

(88.1)

170.6

(74.0)

1,212

914

32.6

PAT before extra-ordinary item

1,344

1,729

(22.2)

1,962

(31.5)

7,836

5,657

38.5

Minority interest(MI)

(41)

7

-

248

-

(10)

1

-

Reported PAT

1,385

1,722

(19.5)

1,714

(19.2)

7,846

5,655

38.7

Adj. PAT

1,385

1,722

(19.5)

1,714

(19.2)

7,846

6,248

25.6

Adj. EPS (`)

5.8

7.2

7.1

32.6

26.0

Source: Company, Angel Research

Exhibit 2: 4QFY2017 - Actual V/s Angel estimates

(` cr)

Actual

Estimates

Variance (%)

Net sales

6,825

7,600

(10.2)

Other income

536

185

189.4

Operating profit

1,235

2,364

(47.7)

Tax

44

372

(88.1)

Adj. Net profit

1,385

1,443

(4.0)

Source: Company, Angel Research

Numbers lower than expectations: For 4QFY2017, the company posted tepid

numbers. For the quarter, the sales came in at `6,825cr v/s. `7,600cr expected,

registering a yoy dip of 7.9%. India sales at `1,916cr, were up by 10% over

4QFY2016, US finished dosage sales at US$381mn were down by

34% over

4QFY2016. Emerging Markets sales at US$181mn were up by 46% over 4QFY2016.

Rest of World sales at US$109mn grew 38% over 4QFY2016. This growth was partly

driven by the consolidation of the Japan business.

Sales of branded formulations in India for 4QFY2017 stood at `1,916cr, up 10% yoy

and accounted for 28% of total sales. Sun Pharma is ranked No. 1 and holds ~8.6%

market share in the `100,000cr pharmaceutical market as per the March-2017

AIOCD-AWACS report.

Sales in the US came in at US$381mn for the quarter, accounting for 37% of total

sales. Sales in emerging markets were at US$181mn for 4QFY2017, a yoy growth of

46% and accounted for 18% of total sales. Formulation sales in Rest of World (ROW)

markets excluding US and Emerging markets were US$109mn in 4QFY2017, a growth

of 38% yoy and accounted for ~11% of revenues for the quarter.

June 9, 2017

2

Sun Pharma | 4QFY2017 Result Update

The company had a total of 427 ANDAs filed with the USFDA. Currently, ANDAs for

157 products await USFDA approval, including 16 tentative approvals.

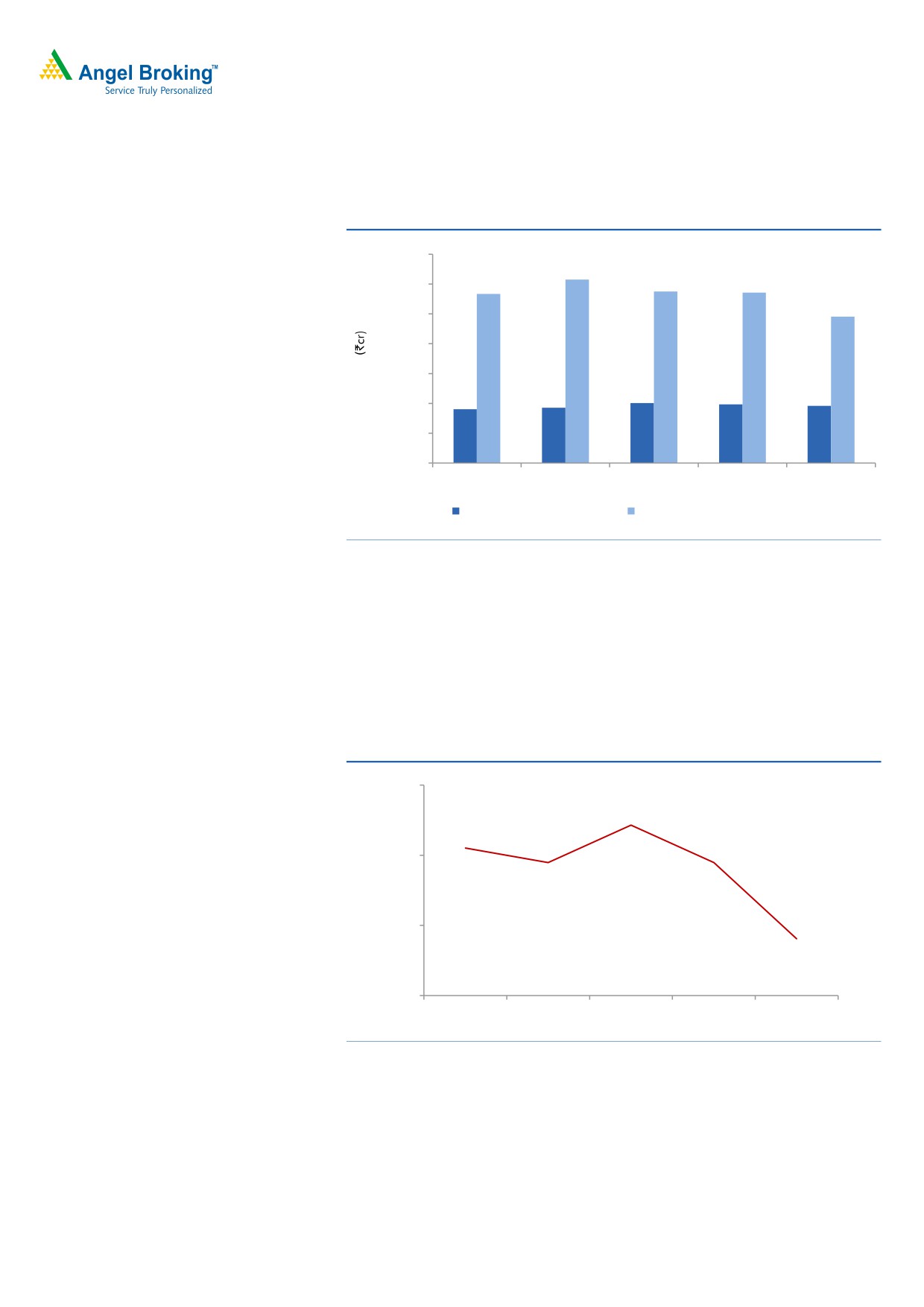

Exhibit 3: Sales trend

7000

6153

5673

5755

5714

6000

4909

5000

4000

3000

2010

1969

1807

1854

1916

2000

1000

0

4QFY2016 1QFY2017 2QFY2017 3QFY2017 4QFY2017

Domestic Formulation

Export Formulation, Bulk and others

Source: Company, Angel Research

OPM at 18.1%, lower than expected: On the OPM front, the gross margins came in at

67.8% v/s. 80.4% in 4QFY2016, which lead the EBDITA margins to come in at 18.1%

(v/s.

31.1% expected) v/s.

31.0% in 4QFY2016. Company’s performance was

impacted by the challenging generic pricing environment in the US. The R&D expenses

came in at 8.8% of sales, almost in-line with last year, at 9.6% of sales as in

4QFY2016.

Exhibit 4: OPM trend (%)

40.0

34.3

31.0

28.9

28.9

30.0

20.0

18.1

10.0

4QFY2016 1QFY2017 2QFY2017 3QFY2017 4QFY2017

Source: Company, Angel Research,

Net profit slightly below expectations: Despite the sharp dip in margins, the higher

other income at `536cr v/s. `185cr in 4QFY2016, lead the Adj. net profit to come

in at `1,385cr v/s. `1,433cr expected, a yoy dip of 19.2%. Other operating

income for the quarter at `312cr included a milestone payment from Almirall S.A.

(Spain), as a part of the licensing agreement for the development and

commercialization of Tildrakizumab for psoriasis in Europe.

June 9, 2017

3

Sun Pharma | 4QFY2017 Result Update

Exhibit 5: Adjusted Net profit trend (` cr)

3,000

2,500

2,235

2,034

2,000

1,714

1,472

1,385

1,500

1,000

500

0

4QFY2016 1QFY2017 2QFY2017 3QFY2017 4QFY2017

Source: Company, Angel Research

Concall takeaways

Revenue may decline due to challenges in the US (assuming no new approval

from Halol and no disruption at Dadra).

Two thirds of Ranbaxy integration benefit came in FY2017; rest expected in

FY2018.

Tildrakizumab NDA launch expected by early 2019.

Gleevec launch in FY2018E.

Investment arguments

Strongest ANDA pipeline: Sun Pharma, with the recent acquisitions of DUSA, URL

Pharma and Ranbaxy Laboratories, has now become strong in the US region, with

the geography accounting for 37% of its sales in FY2017. In terms of ANDAs, the

company cumulatively has 427 products, out of which 157 products now await

USFDA approval, including 16 tentative approvals. With the merger of Ranbaxy

Laboratories, the company is now the fifth-largest specialty generics company in

the world (behind Teva, Sandoz, Activas and Mylan). However, the near term

performance of the company has been impacted on the back of supply constraints

at the Halol facility although the company has taken redemption measures

including site transfers. Overall, we expect the region to post a CAGR of 6.4% in

sales over FY2017-19E, accounting for almost 44% of the overall sales in

FY2019E.

Domestic business: Sun Pharma’s domestic formulation business is among the

fastest growing in the Indian pharmaceutical industry. It contributed 23% to the

company’s total turnover in FY2014. Sun Pharma, with Ranbaxy Laboratories’

merger, is now the segment leader with a market share of 8.7% in the domestic

formulation market, followed by Abbott India, which has a market share of 6.5%.

This is a significant gap considering that the segment is highly fragmented. We

expect the domestic formulation business to post a CAGR of

14.5% over

June 9, 2017

4

Sun Pharma | 4QFY2017 Result Update

FY2017-19E, contributing 28% to the overall formulation sales of the company in

FY2019.

Healthy balance sheet: Sun Pharma has one of the strongest balance sheets in the

sector with cash of

~`15,000cr. The same can continue to support the

Management in inorganic growth and in scouting for acquisitions, especially in the

US and in emerging markets.

Outlook and valuation: Sun Pharma is one of the largest and fastest growing

Indian pharmaceutical companies. We expect its net sales to post a CAGR of 9.7%

(including Ranbaxy Laboratories) to `36,451cr and EPS to post a CAGR of (0.5)%

to `32.3 over FY2017-19E. We recommend a Buy rating on the stock.

Exhibit 6: Key assumptions

FY2018E

FY2019E

Domestic Formulation sales growth (%)

14.0

15.0

Export Formulation sales growth (%)

8.9

9.9

Growth in employee expenses (%)

20.0

20.0

Operating margins (%)

26.9

25.4

Tax as % of PBT

15.0

15.0

Source: Company, Angel Research

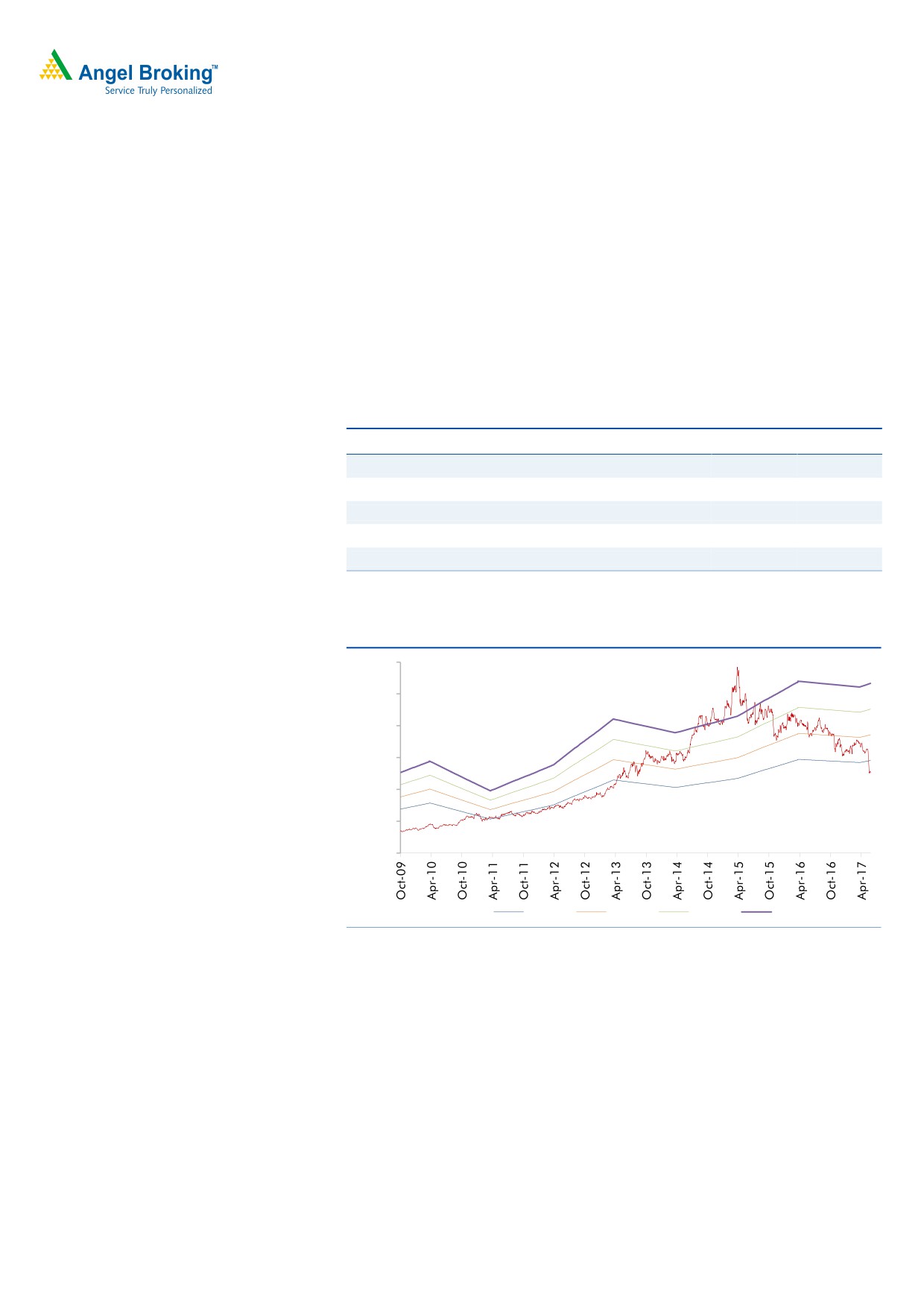

Exhibit 7: One-year forward PE band

1,200

1,000

800

600

400

200

-

10x

15x

20x

25x

Source: Company, Angel Research

June 9, 2017

5

Sun Pharma | 4QFY2017 Result Update

Exhibit 8: Valuation summary

Company

Reco

CMP

Tgt. Price

Upside

FY2018E

FY16-18E

FY2018E

(`)

(`)

% PE (x) EV/Sales (x) EV/EBITDA (x) CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Buy

552

648

17.3

21.7

2.5

12.0

(10.8)

27.5

25.3

Aurobindo Pharma

Buy

609

823

35.2

13.6

2.2

9.9

18.1

22.5

26.1

Cadila Healthcare

Sell

541

450

(16.8)

28.4

4.8

23.8

(0.5)

16.2

24.6

Cipla

Sell

550

465

(15.5)

22.4

2.5

15.2

14.2

12.2

13.9

Dr Reddy's

Neutral

2,631

-

-

24.8

2.9

15.8

(13.7)

10.8

13.6

Dishman Pharma

Under Review

301

-

-

26.6

2.9

12.7

16.3

13.0

13.5

GSK Pharma*

Neutral

2,463

-

-

49.7

6.2

38.4

6.0

22.3

21.3

Indoco Remedies

Sell

193

153

(20.7)

17.1

1.7

11.7

6.3

10.1

15.0

Ipca labs

Buy

501

710

41.7

25.8

1.8

12.6

13.9

10.4

9.5

Lupin

Buy

1,161

1,526

31.5

19.0

2.7

11.4

10.0

20.6

17.8

Sanofi India

Neutral

4,051

-

-

29.0

3.3

19.8

16.8

22.5

26.4

Sun Pharma

Buy

525

712

35.7

16.6

3.5

12.9

1.2

16.9

18.7

Source: Company, Angel Research; Note: * December year ending

Company background

Sun Pharma is an international specialty pharma company, with a large presence

in the US and India, and a footprint across 40 other markets. In India and rest of

the world markets, the key chronic therapy areas for the company are cardiology,

psychiatry, neurology, gastroenterology, diabetology, etc. The company is a

market leader in specialty therapy areas in India. In India, the company has

emerged as a leading pharma company, where it is the third largest player. Also,

in the US, a key geography, the company has expanded significantly through both

in-organic and organic routes.

June 9, 2017

6

Sun Pharma | 4QFY2017 Result Update

Profit & Loss statement (Consolidated)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Gross sales

27,652

28,254

30,536

33,198

36,782

Less: Excise duty

366

366

272

299

331

Net sales

27,287

27,888

30,264

32,899

36,451

Other operating income

147

599

1,314

1,314

1,314

Total operating income

27,433

28,487

31,578

34,213

37,765

% chg

70.6

3.8

10.9

8.3

10.4

Total expenditure

19,470

21,014

21,489

24,054

27,193

Net raw materials

6,739

6,330

8,131

8,839

9,793

Other mfg costs

1,192

1,218

1,322

1,437

1,593

Personnel

4,430

4,772

4,902

5,883

7,059

Other

7,109

8,693

7,134

7,896

8,748

EBITDA

7,817

6,874

8,775

8,845

9,258

% chg

12.9

(12.1)

(27.5)

(34.4)

34.7

(% of Net Sales)

28.6

24.6

29.0

26.9

25.4

Depreciation & amort.

1,195

1,038

1,265

1,465

1,665

EBIT

6,622

6,436

8,825

8,694

8,907

% chg

1.7

(2.8)

(18.7)

(1.5)

2.5

(% of Net Sales)

24.3

23.1

29.2

26.4

24.4

Interest & other charges

579

523

400

400

400

Other income

451

1,248

623

623

623

(% of PBT)

6.8

17.4

6.9

7.0

6.8

Share in profit of Asso.

-

-

-

1.0

Recurring PBT

6,641

7,161

9,048

8,917

9,131

% chg

-6.4

7.8

-16.8

0.0

0.1

Extraordinary expense/(inc.)

237.8

589.9

-

-

1.0

PBT (reported)

6,641

7,161

9,048

8,917

9,130

Tax

914.7

913.8

1,211.6

1,337.6

1,369.4

(% of PBT)

13.8

12.8

13.4

15.0

15.0

PAT (reported)

5,726

6,247

7,836

7,580

7,760

Add: Share of earnings of asso.

(13)

1

10

-

-

Less: Minority interest (MI)

936

-

-

-

-

Prior period items

-

-

-

-

PAT after MI (reported)

4,539

5,658

7,846

7,580

7,760

ADJ. PAT

4,743

6,248

7,846

7,580

7,760

% chg

(10.0)

31.7

65.4

(3.4)

2.4

(% of Net Sales)

16.6

0.0

1.0

2.0

3.0

Basic EPS (`)

22.9

26.0

32.7

31.6

32.3

Fully Diluted EPS (`)

22.9

26.0

32.7

31.6

32.3

% chg

(10.0)

13.4

42.8

(3.4)

2.4

June 9, 2017

7

Sun Pharma | 4QFY2017 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

SOURCES OF FUNDS

Equity share capital

207

241

240

240

240

Preference capital

Reserves & surplus

26,300

32,742

36,400

42,857

49,494

Shareholders’ funds

26,507

32,982

36,640

43,097

49,734

Minority interest

2,851

4,085

3,791

3,791

3,791

Total loans

7,596

8,316

8,091

8,091

8,091

Deferred tax liability

(1,752)

(3,046)

(2,178)

(2,178)

(2,178)

Other Long Term Liabilities

9

-

-

-

-

Long Term Provisions

2,710

2,106

1,342

2,523

2,853

Total liabilities

37,922

44,443

47,685

55,324

62,290

APPLICATION OF FUNDS

Gross block

15,041

15,084

18,162

19,162

20,162

Less: Acc. depreciation

4,863

7,139

8,404

9,869

11,534

Net block

10,179

7,945

9,758

9,293

8,628

Capital work-in-progress

842

842

303

303

303

Goodwill

3,701

9,261

10,417

10,417

10,417

Investments

2,716

1,830

1,192

1,388

1,389

Long term long & adv.

2,736

3,276

4,526

4,574

5,068

Current assets

27,005

29,227

32,723

38,436

46,757

Cash

10,998

13,182

15,141

19,178

25,420

Loans & advances

2,193

2,006

2,480

2,696

2,987

Other

13,813

14,040

15,102

16,562

18,351

Current liabilities

9,256

7,938

11,232

9,086

10,272

Net current assets

17,748

21,290

21,491

29,350

36,486

Others

-

-

-

-

-

Total assets

37,922

44,443

47,685

55,324

62,290

June 9, 2017

8

Sun Pharma | 4QFY2017 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Profit before tax

6,641

7,161

9,048

8,917

9,131

Depreciation

1,195

1,038

1,265

1,465

1,665

(Inc)/Dec in working capital

(4,322)

(1,898)

(2,505)

(14,746)

(4,750)

Direct taxes paid

915

914

1,212

1,338

1,369

Cash Flow from Operations

2,598

5,386

6,596

(5,702)

4,676

(Inc.)/Dec.in Fixed Assets

(8,653)

(43)

(1,682)

(1,000)

(1,000)

(Inc.)/Dec. in Investments

70

886

1,524

(196)

(1)

Other income

-

-

-

-

-

Cash Flow from Investing

(8,583)

843

(157)

(1,196)

(1,001)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(4,928)

(1,333)

(1,873)

1,181

329

Dividend Paid (Incl. Tax)

-

(282)

(1,123)

(1,123)

(1,123)

Others

14,320

(2,431)

(1,485)

10,875

3,360

Cash Flow from Financing

9,392

(4,046)

(4,480)

10,934

2,566

Inc./(Dec.) in Cash

3,408

2,184

1,959

4,036

6,242

Opening Cash balances

7,590

10,998

13,182

15,141

19,178

Closing Cash balances

10,998

13,182

15,141

19,178

25,420

June 9, 2017

9

Sun Pharma | 4QFY2017 Result Update

Key Ratios

Y/E March

FY2015

FY2016

FY2017

FY2018E

FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

22.9

20.2

16.0

16.6

16.2

P/CEPS

19.0

18.9

13.8

13.9

13.4

P/BV

4.8

3.8

3.4

2.9

2.5

Dividend yield (%)

0.6

0.2

0.2

0.2

0.2

EV/Sales

3.9

4.4

3.9

3.5

3.0

EV/EBITDA

13.5

17.7

13.6

13.1

11.9

EV / Total Assets

2.8

2.7

2.5

2.1

1.8

Per Share Data (`)

EPS (Basic)

22.9

26.0

32.7

31.6

32.3

EPS (fully diluted)

22.9

26.0

32.7

31.6

32.3

Cash EPS

27.7

27.8

38.0

37.7

39.3

DPS

3.0

1.0

1.0

1.0

1.0

Book Value

110.2

137.1

152.3

179.1

206.7

Dupont Analysis

EBIT margin

24.3

23.1

29.2

26.4

24.4

Tax retention ratio

86.2

87.2

86.6

85.0

85.0

Asset turnover (x)

1.2

1.0

1.1

1.0

1.0

ROIC (Post-tax)

26.1

19.7

27.5

22.4

21.5

Cost of Debt (Post Tax)

9.8

5.7

4.4

8.4

4.1

Leverage (x)

0.0

0.0

0.0

0.0

0.0

Operating ROE

26.1

19.7

27.5

22.4

21.5

Returns (%)

ROCE (Pre-tax)

21.1

15.6

18.8

16.9

15.1

Angel ROIC (Pre-tax)

38.3

29.6

41.3

36.8

34.5

ROE

21.1

21.0

22.2

18.7

18.8

Turnover ratios (x)

Asset Turnover (Gross Block)

2.6

1.9

1.9

1.8

1.9

Inventory / Sales (days)

58

77

76

82

90

Receivables (days)

50

76

76

82

90

Payables (days)

61

91

95

69

69

WC cycle (ex-cash) (days)

82

95

71

54

93

Solvency ratios (x)

Net debt to equity

(0.1)

(0.1)

(0.2)

(0.3)

(0.3)

Net debt to EBITDA

(0.4)

(0.7)

(0.8)

(1.3)

(1.9)

Interest Coverage (EBIT/Int.)

-

-

-

-

-

June 9, 2017

10

Sun Pharma | 4QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Sun Pharma

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

Yes

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

June 9, 2017

11